Summary

Extends the IS-LM model by incorporating real interest rates, expected inflation, and risk premia into the IS relation. The nominal-real interest rate distinction matters because private sector decisions depend on , not . Adding a risk premium driven by default probability further adjusts the rate firms face. Both channels modify the IS curve: higher or lower shift IS right, mimicking expansionary monetary policy.

Nominal vs. Real Interest Rates

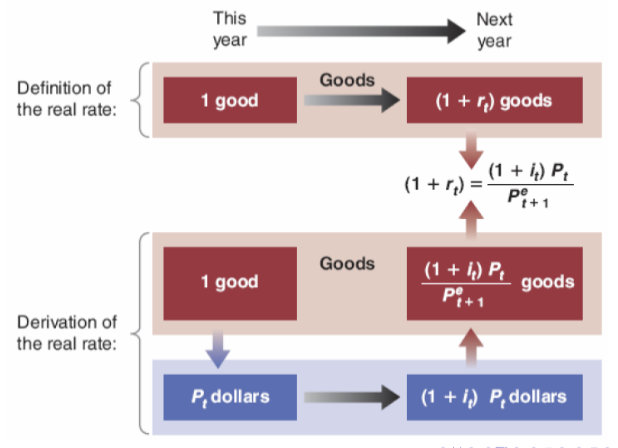

Nominal interest rate () is in terms of dollars, while real interest rate () is the interest rate in terms of a basket of goods. Ex-ante, the difference is expected inflation. We care about this distinction because private sector decisions (like investment) depend on real interest rate.

Note that we cannot predict the future, so the interest rate is expected. The one-year real interest rate at time , , can be modeled as:

Note that we cannot predict the future, so the interest rate is expected. The one-year real interest rate at time , , can be modeled as:

We denote the expected inflation as

to imply approximately:

Risk and Risk Premium

Some bonds are risky, so bond holders have a risk premium (the credit spread) to hold these bonds :

This moves a lot and tends to be higher during recessions. We care because private sector decisions depend on risk-adjusted interest rate.

The risk premium is determined by the probability of default and the degree of risk aversion of bond holders. We’ll ignore the second channel and denote the probability of default as . Then we have

which implies

During recessions, can rise a lot, so goes up.

Expanded IS-LM

Let’s expand the IS-LM model to incorporate these new ideas. Everything new is in the IS relation:

If declines or rises:  as if we had an expansionary monetary policy. Conversely, if rises and/or falls, we have the opposite effect.

as if we had an expansionary monetary policy. Conversely, if rises and/or falls, we have the opposite effect.