Summary

The underlying issue is how to decide what the current price of an asset is and whether it’s consistent with the future cash flows generated by that asset. The answer involves expectations (the expected part of EPDV) and some method to compare payments received in the future with those made today (the PDV part).

Note

The word discounted means payments received in the future are worth less than those received today.

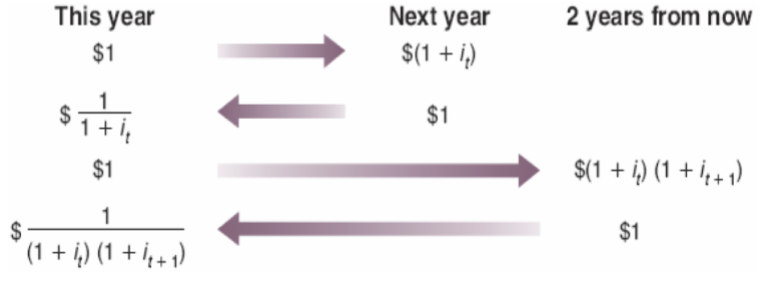

Let’s simplify and assume we know the future.  We want to decide how much we would want to pay for a bond today to receive $1 in X years. The general formula for the present discounted value is:

We want to decide how much we would want to pay for a bond today to receive $1 in X years. The general formula for the present discounted value is:

Each future payment is discounted by the product of all intervening one-year interest rates . A dollar next year is worth today, a dollar two years out is worth , and so on.

If we do not know the future, we replace future values with their expectations, taken as of time (written ):

Both the future payments and the future interest rates are now expected values. This is the expected present discounted value (EPDV).

If we have a constant interest rate , this simplifies to:

And if payments are also constant ( for all ), the geometric series gives:

If payments start next year (no payment at time ):

If goes to zero, the asset values go to infinity.

Bond Prices & Yields

Bonds differ in maturity.

Example

A bond promising to make a $1k payment in 6 months has a maturity of 6 months.

Bonds of different maturities have a yield. In general, the longer the bond, the higher the rate, but this often isn’t the case, especially in inflationary periods.

Arbitrage implies that bond prices should be such that you are indifferent between investing in a 1 year bond, for instance, rather than investing in a 2 year bond and selling it after 1 year. In other words,

The yield to maturity on an n-year bond is the constant annual interest rate that makes the bond price today equal to the PDV of future payments of the bond. For instance:

which implies

Bond Risk

Bonds have two types of risk:

- Default risk, which is how likely the issuer won’t pay back the amount promised

- Price risk, which is uncertainty about the price at which you can sell the bond if you sell it before maturity.

Suppose we invest in highly rated bonds so that the default risk is low, and we can still choose between 1y and 2y bond.

This also implies the yield to maturity has a risk premium (term premia):

Stock Prices

Stocks pay dividends which vary over time and do not have a fixed terminal date. We can price a stock by arbitrage, assuming the investor can opt between a 1y bond and stocks:

We can rearrange to find the price . We can also derive the expression in real terms in a similar way.

When there is monetary expansion, the interest rate goes down so bond prices go up, and other things equal, stock prices also go up.  An increase in consumer spending leads interest rates to go up, which lowers the price of bonds.

An increase in consumer spending leads interest rates to go up, which lowers the price of bonds.