Summary

The basic IS-LM model overhypes the present. In practice, expectations about future conditions play a big role in all economic decisions.

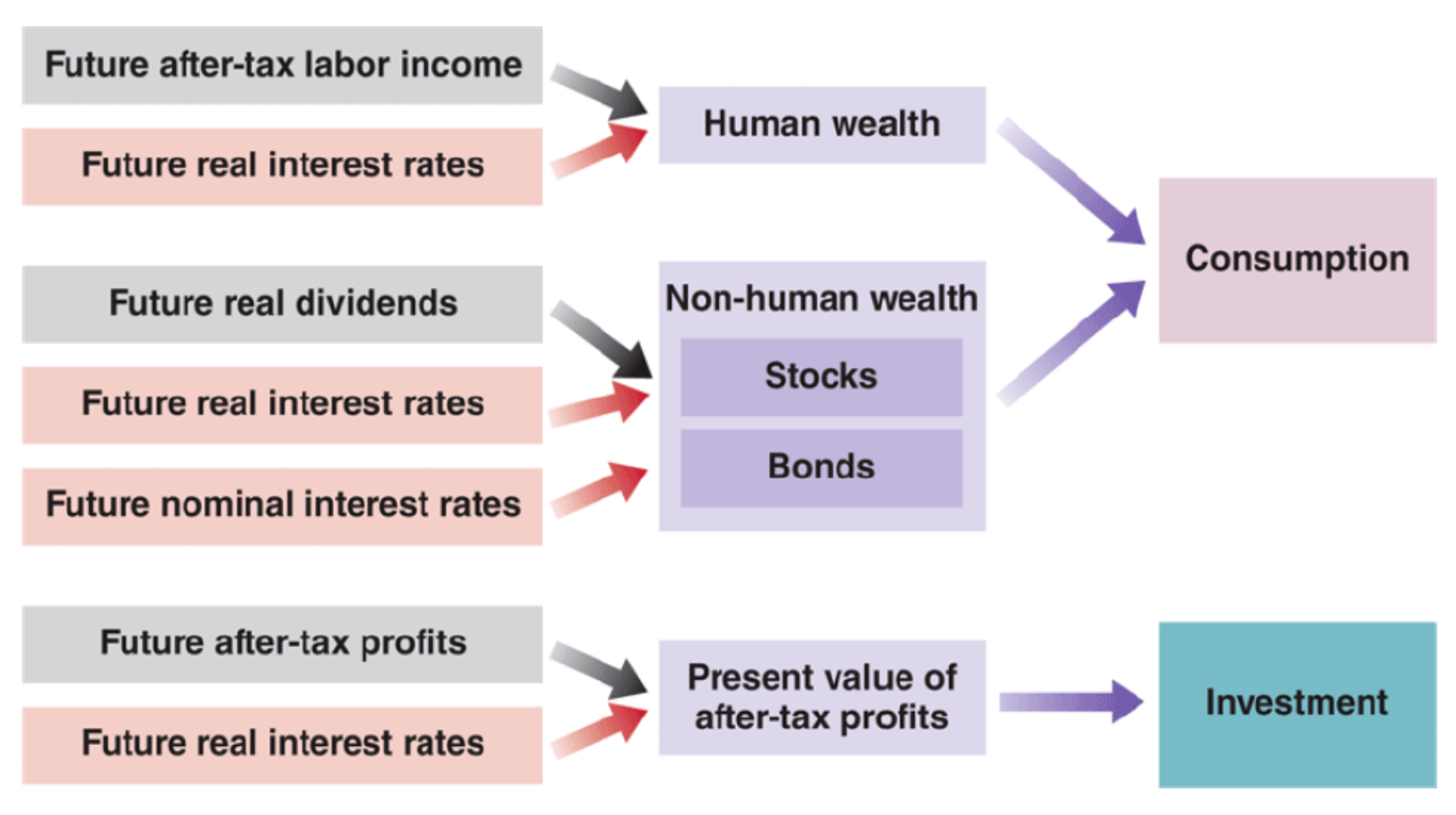

Consumption

Consumption decisions depend not just on current income but on expected future income/wealth. Two predominant theories:

- Permanent income theory of consumption (Friedman)

- Life-cycle theory of consumption (Modigliani)

Total wealth includes financial wealth (value of all assets minus debt, as EPDV) and human wealth (EPDV of labor income). In principle,

In practice,

This accounts for the distinction between permanent versus temporary changes in income.

Investment

Investment decisions depend on both current and expected profits and interest rates. Firms weigh their decision against the EPDV of the profits it will generate.

Depreciation captures how long an asset lasts and how much value it retains. A reasonable assumption is geometric depreciation, modeled as each year. The PV of expected profits:

In principle,

but in practice:

Note

Persistently higher profits matter more than transitory ones.

IS-LM with Expectations

A shortcut to the IS-LM model with expectations:

A shortcut to the IS-LM model with expectations:

The LM relation stays the same: .